Tax-efficient

Your deposit is deductible within your annual allowance

Customisation

A fully personalised strategy — no standard A/B/C profiles.

Always insightful

Real-time insight into how your money is working — via the Vive app.

Tax-efficient

Your deposit is deductible within your annual allowance

Customisation

A fully personalised strategy — no standard A/B/C profiles.

Always insightful

Real-time insight into how your money is working — via the Vive app.

As a self-employed professional or freelancer, you want flexibility in your investments — the freedom to take breaks when needed and make additional contributions at the end of the year. Vive adapts to your rhythm.

Your business doesn't have to be the only pot you build. As a Director-Owner, you accrue your own pension. Deposit money every month and build up a pension step by step.

Important: Your pension pot is in your name. Always.

Even if you return to employment later.

Blocked until retirement, with tax benefits

Flexible access, no tax benefits

Complex pension, simply explained

Our free pension brochure helps you easily understand how to build a pension as an entrepreneur.

How to arrange your pension entirely via Vive, in one app

How easy and fast our onboarding process is

How we offer competitive pricing with no hidden costs

In your mailbox within 1 minute

Contributions made within available annual and carryforward allowance are deductible from your taxable income. Part of the contribution is refunded on your tax return.

Your pension account is excluded from Box 3. No wealth tax is due on your assets during the accumulation phase.

During the payout phase, your pension income is taxed — but usually at a lower tax rate than today. This means you keep more net income.

Would you like to learn more about your annual allowance and the benefits of pension investing? Feel free to schedule a free appointment with one of our experts.

* For the indicative tax refund, we use the 2025 rates. These are bracket 1: Up to €38,441, a rate of 35.82%; bracket 2: Between €38,441 and €76,817, a rate of 37.48%; bracket 3: For incomes above €76,817, a rate of 49.50%. The actual amount you get back depends on your personal situation. Terms apply.

Schedule a free appointment. We’ll discuss your goals, income, and risk preferences. You can then easily open your pension account online (±5 minutes) and sign the agreement.

You’ll receive an invitation to the Vive app. Download the app, log in, and complete the onboarding process. We’ll then carry out a quick identity check (required by law), after which you can get started.

Your retirement account is active. Make contributions whenever it suits you — manually or via recurring payments. Easily track your progress in the app.

Would you like to schedule an appointment for more information, or get started right away? Our pension experts are happy to help.

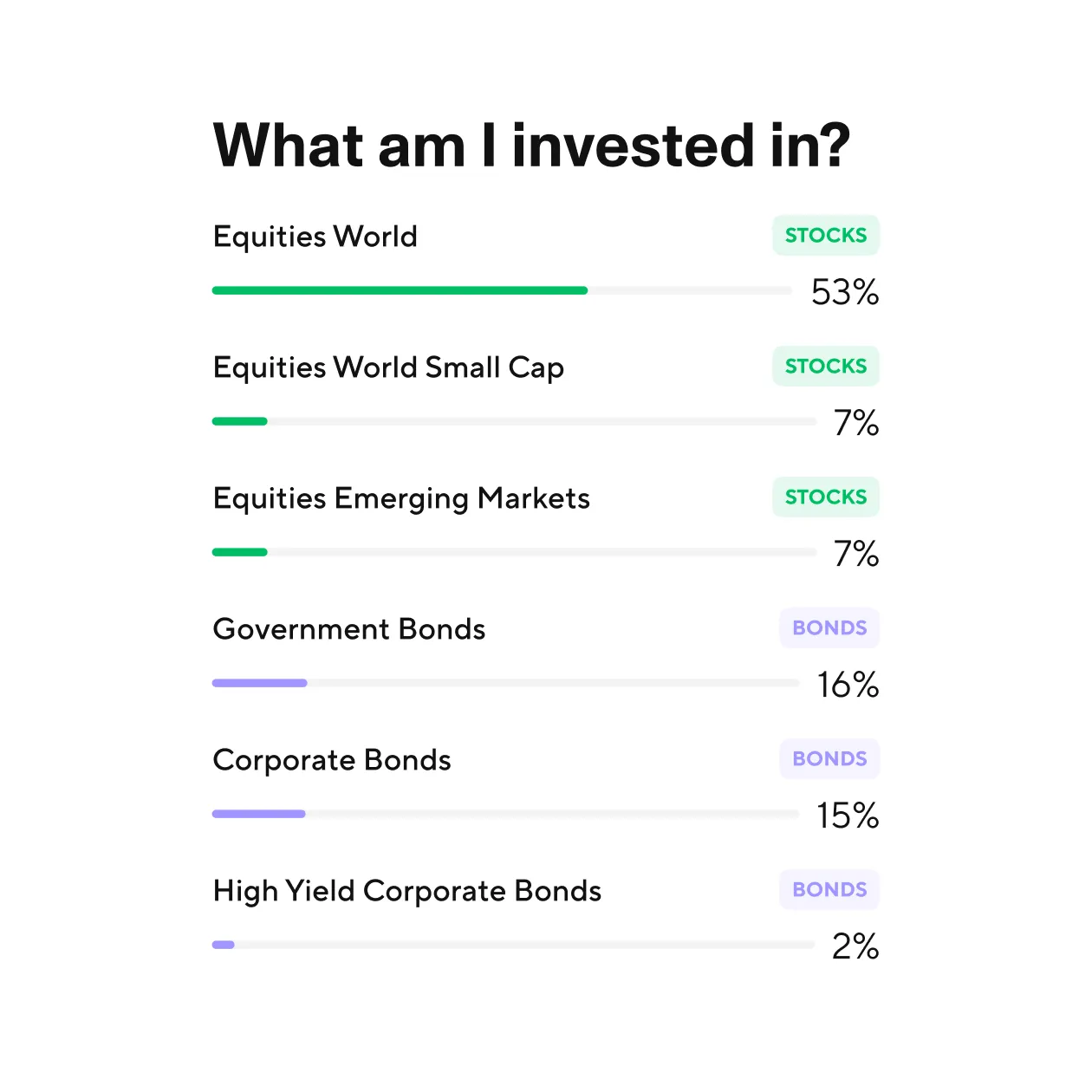

Vive invests on your behalf in passive index funds. Spanning thousands of companies across multiple sectors. Fully ESG-screened, at low cost.

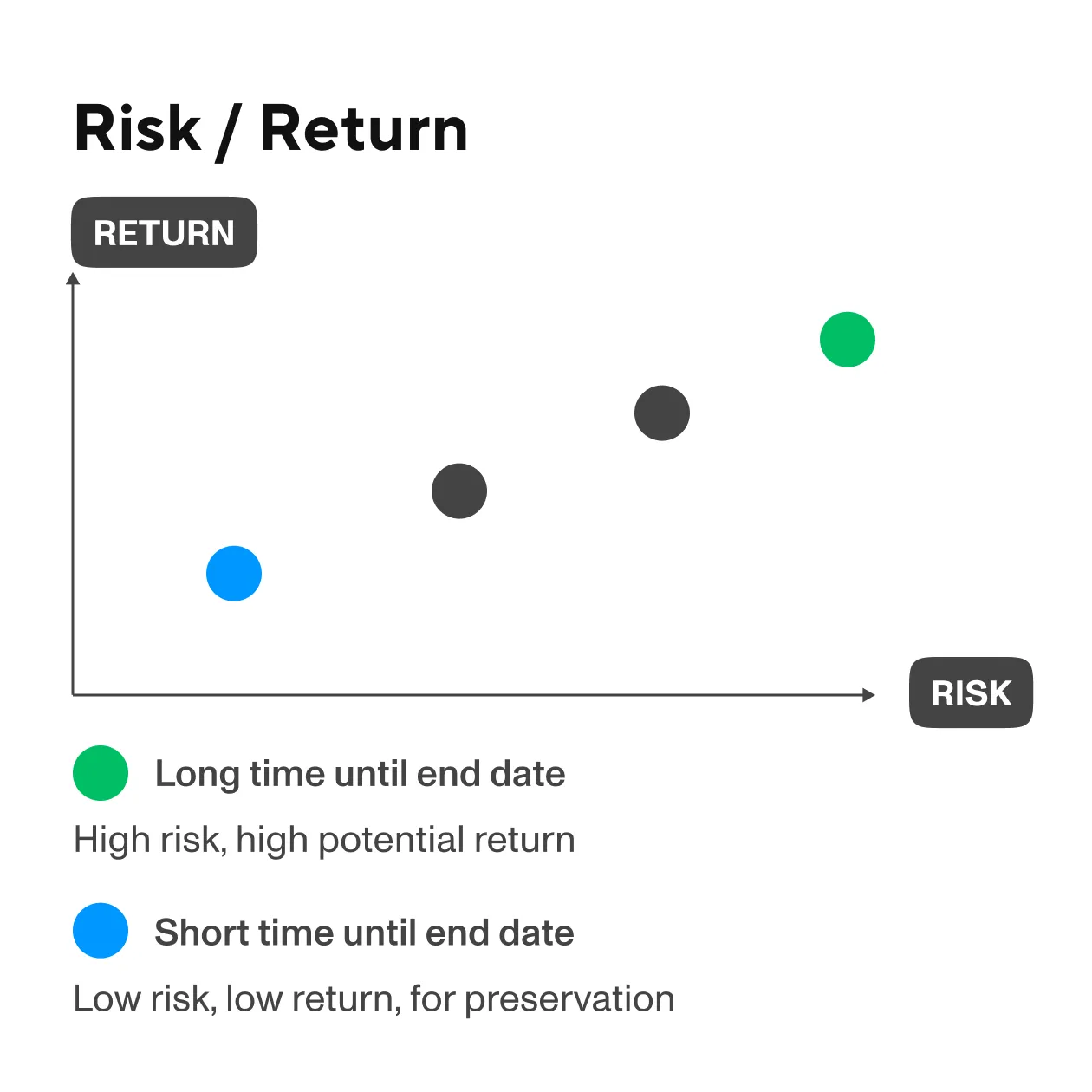

Risk is gradually reduced as you near retirement — maximising growth during accumulation and protecting your assets during decumulation.

As markets move, your portfolio adapts — without you having to do anything. This is how we maintain your personal strategy.

While most investment providers rely on standard profiles, Vive works differently. We build a strategy based on your goals, time horizon, and personal situation — not a one-size-fits-all solution.

As a director-owner, you pay yourself a customary salary from your company and are legally considered an employee.

Contributions must be made from your net salary to qualify for the tax benefit.

You can pay both the monthly and one-off costs through your company and include them as operating expenses.

Important: Always make pension contributions from your personal account — not directly from your company or holding company. Otherwise, you will lose the tax benefit entirely. Want to learn more?

“What sets Vive apart from other pension solutions is that you have a lot of freedom in the plan that you can use. You can provide much more customization.”

Ready for a modern pension or wealth solution? Get to know Vive and discover what’s possible — for you.

Complex pension, simply explained - so you know exactly where you stand

A personal consultation tailored to your situation

More clarity in 30 minutes than hours of Googling

Everything you need. In one app. In one place. All goals and strategies, always at hand.

A pension solution specifically for majority shareholders/managing directors. Because you are not an employee, you have to arrange this yourself. Via Vive, you can do this easily, with tax advantages and completely at your own pace.

You deposit from your net salary into a pension account. The money is invested and grows until you reach retirement age. In the Vive app, you can see exactly where you are standing.

Yes, in many cases, this is possible. DGA pension is deductible within your annual margin. What you deposit within your annual space is deducted from your taxable income. You will receive part back immediately via your declaration.

While each pension investment party offers tax benefits, Vive gives you more thanks to low investment costs and the elimination of transaction and deposit costs. In addition, your investment is fully invested through a customized, personal strategy. This allows you to benefit from professional asset management at the low, transparent rates of major pension funds. This results in better conditions for your own pension pot, without being bound by strict rules.

If you are in paid employment, your pension is often part of a collective scheme through your employer. The accrual happens automatically, and you have little influence over it yourself. For self-employed individuals (zzp’ers), there is no standard scheme: you must arrange your own pension accrual. At Vive, you do this through your own pension account, where you can make flexible contributions and arrange everything yourself. Simple, insightful, and with smart investment strategies.

Yes. Your investments are held by an independent custody company, separate from Vive. In the event of bankruptcy, your money remains protected.

Investing offers opportunities, but you may lose part or all of your investment. That’s why it’s important to understand the associated risks in advance. More information can be found in the Investment Policy. Vive is a licensed wealth manager.