Wat is flexibel pensioen van Vive?

Fully tailored to your needs.

Vive is a third-pillar pension solution. It’s not a traditional industry-wide pension fund or collective scheme, but a modern, individual pension account (also known as a personal pension or annuity account) that you, as an employer, can sponsor for your team. You decide when to contribute, for whom, and how much.

Scenario 1: Mandatory industry pension scheme (BPF/CAO)

Vive is an excellent supplement. Your employees build up additional pension savings alongside their mandatory scheme, with tax advantages.

Scenario 2: No mandatory (or industry) pension scheme

Vive can serve as your primary pension solution. Offer a modern pension plan without the complexity and costs of a collective fund.

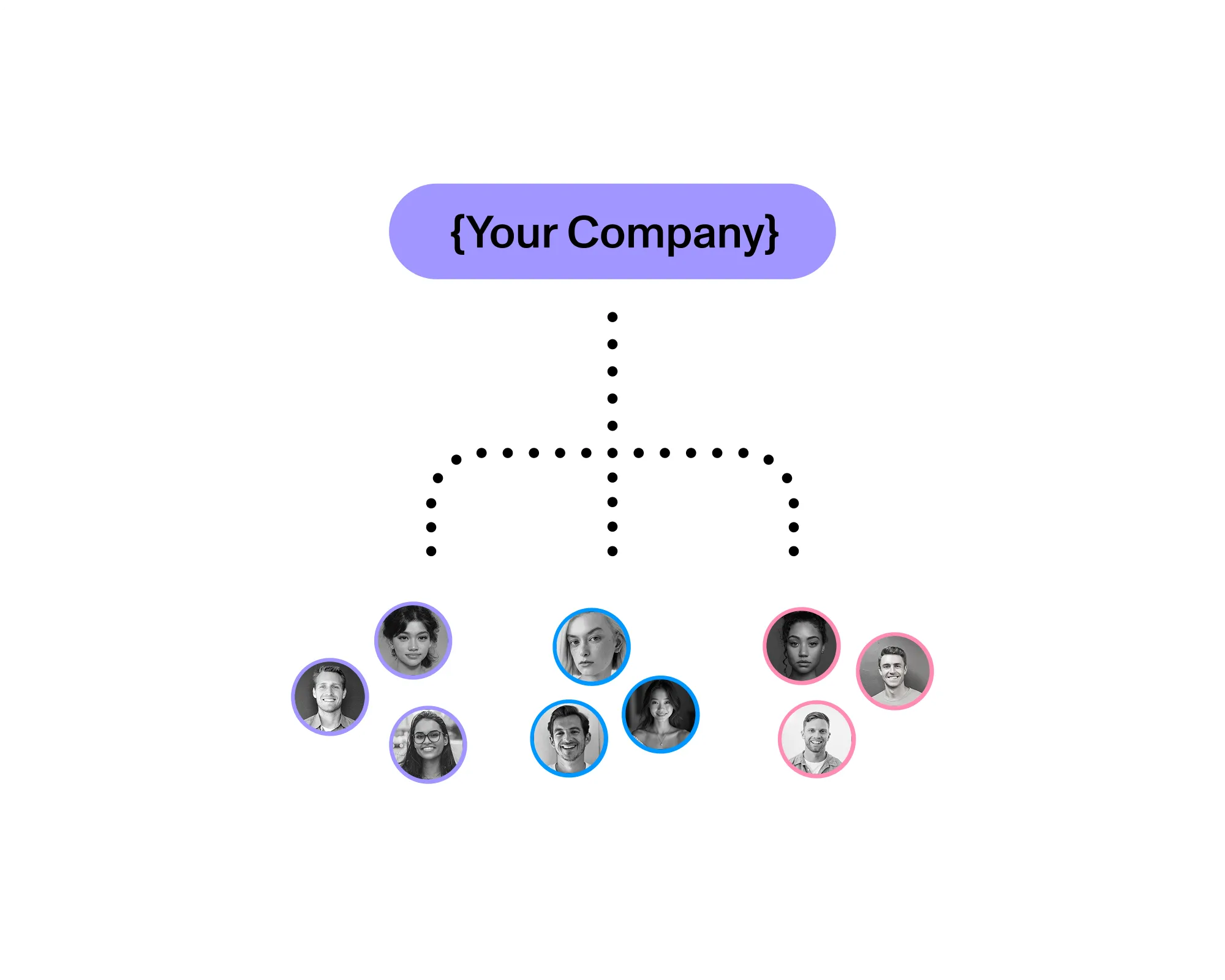

How Vive works

For you as an employer - and for your employees.

For you as an employer

What you do

For your employees

What they get

Elke werkgever stelt pensioen anders in

Dit zijn enkele opties hoe het kan werken.

Set up in 3 steps

From the first meeting to a live pension plan. No hassle.

Getting to know you

We discuss your wishes, decide who will participate and what you want to contribute for whom. After that, we sign the cooperation agreement.

Onboarding

We organize onboarding for your team: digitally or on location. Everyone gets an explanation, access to the app and a personal customer success manager.

Your pension is live

All accounts are activated, with a clear overview in the dashboard. You decide who to sponsor and how much to contribute each month. All set, for your employees and yourself.

Complex pension, simply explained

Want to know more about our pension plan?

Our brochure explains clearly how Vive's pension plan works. No hassle, just clarity.

Among other things, you will read:

How to fully arrange your pension via Vive in one app

How easy and fast our onboarding process works

How we offer a competitive price without hidden costs

In your mailbox within 1 minute

Everything arranged via one portal

Manage all pension plans in just a few minutes per month.

Managing teams and employees

Add employees, track the invitation status, and arrange onboarding and offboarding in just a few clicks.

Set up a deposit per employee

Organize the contribution per person, team or specific contract type. Choose a percentage or fixed amount, with optional matching.

Multiple arrangements possible

From standard pension plans to one-off bonus plans. Assign specific arrangements to employees or simply modify existing ones.

How it works on the payslip

Employers can contribute directly to employees’ annuity accounts while retaining tax benefits.

Net salary deduction

You deduct the contribution from the employee’s net salary and transfer it directly to Vive. The employee can deduct the contribution for income tax purposes.

Amount treated as final levy item

You designate part of the gross salary as a final tax levy. This amount becomes net pay for the employee and is deductible within the available annual allowance.

Important: The contribution must fall within the employee’s annual and/or carryforward allowance. Always coordinate with your payroll administration or tax advisor.

What your employees get with Vive

A pension they understand, can access at any time, and take with them wherever they go.

Tax advantage

The contribution is tax-deductible and does not count towards wealth tax. Vive automatically reports balances to the tax authorities.

Personal pension pot

The pension is in the employee's name and accompanies a job change. Always grip, always continuity.

More than just pensions

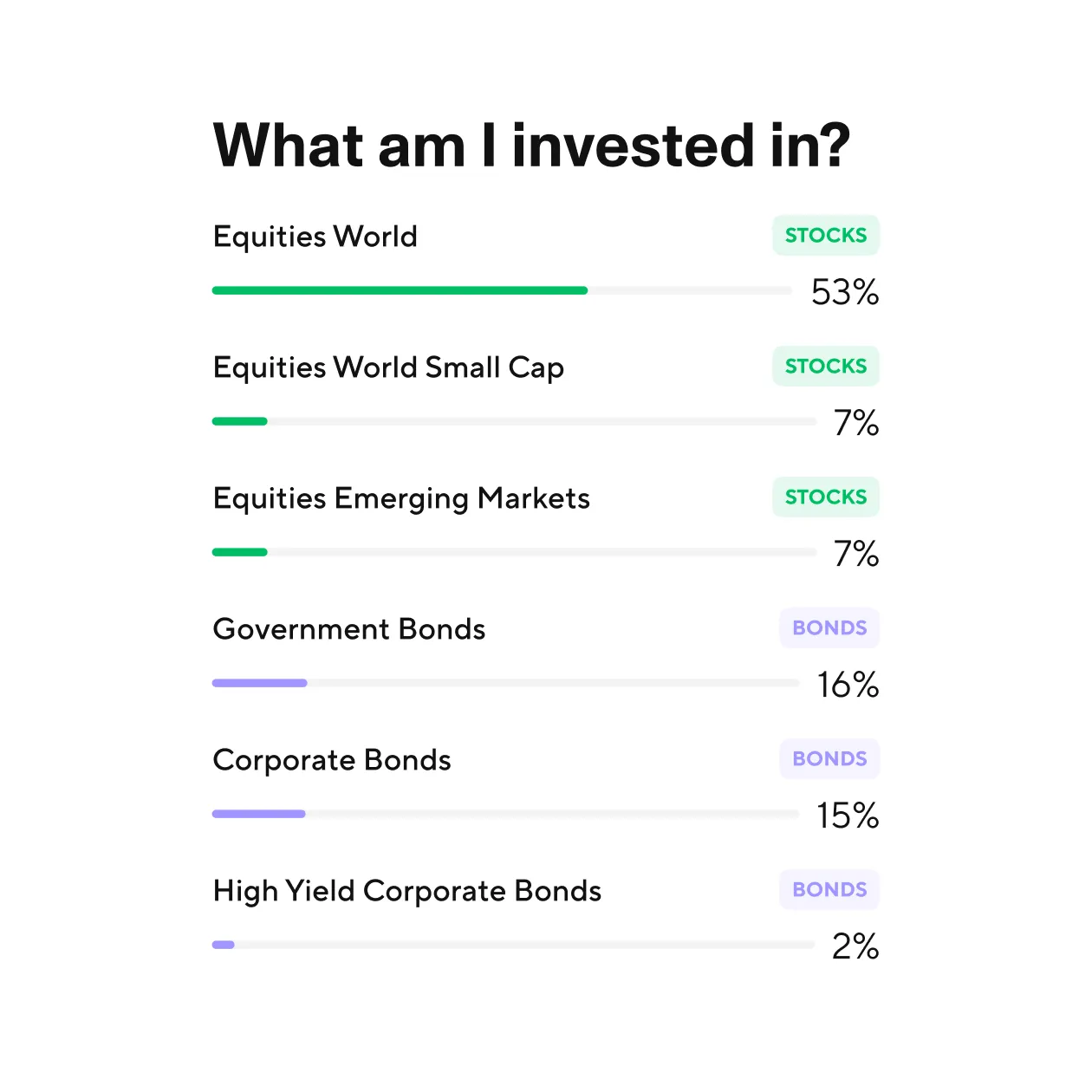

How Vive invests

Professional pension and asset management, now accessible to everyone.

Personal Strategy (ALM)

Vive creates a tailored strategy for each employee, based on their goals, time horizon, personal situation, and market expectations. No standard A/B/C profiles.

Passive & diversified

Vive invests on your behalf in index funds from providers such as Northern Trust and Vanguard. These funds are globally diversified, ESG-screened, and dividend-efficient.

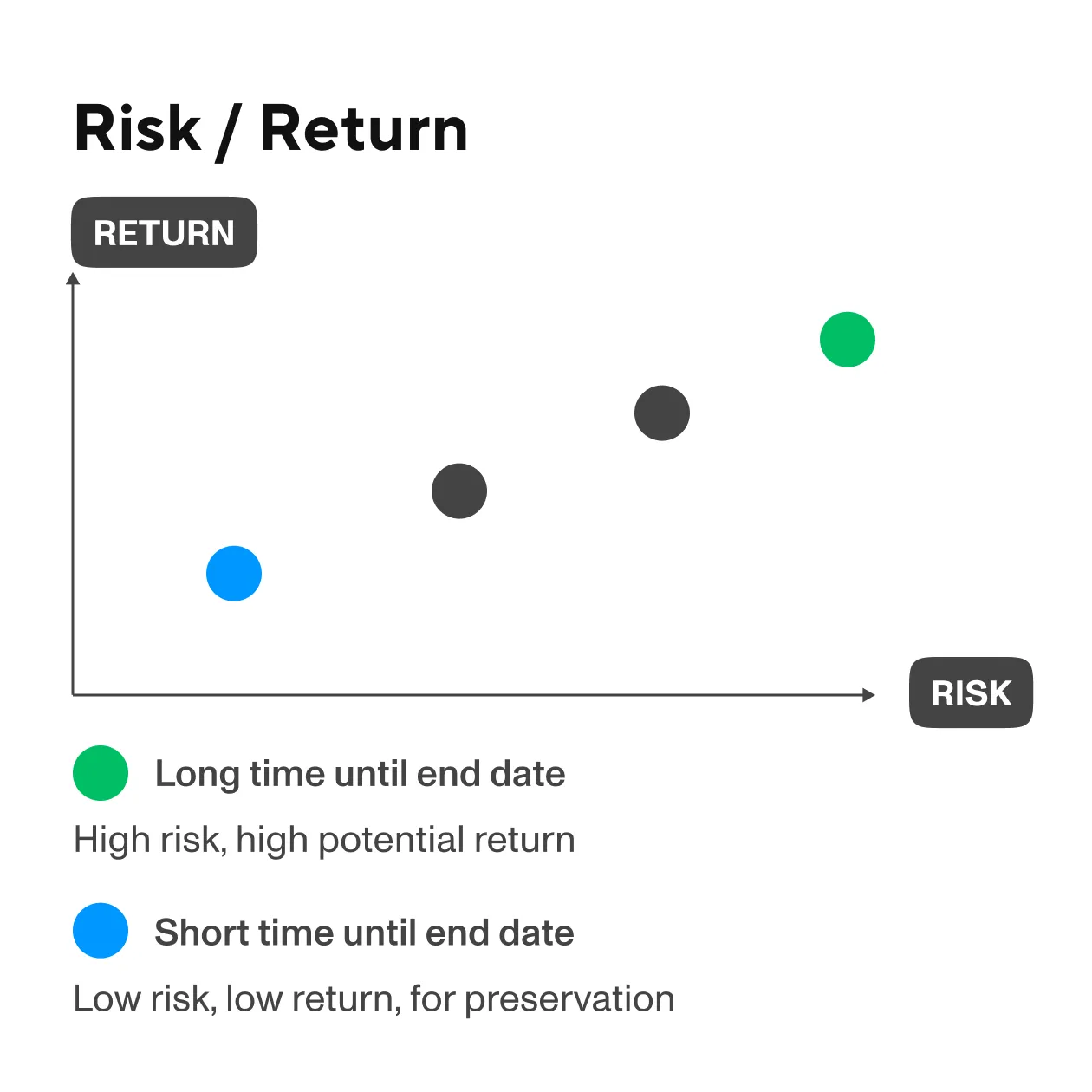

Life-cycle investing

Automatic risk reduction towards retirement. Fewer stocks, more bonds as the retirement date approaches. Optimized based on your life.

Vive invests for each person with a tailored strategy. Personal, diversified and fully optimized.

Your assets and pension

Completely safe and supervised.

Trusted by over 2,500 happy customers

Technology that employers and employees understand.

Vive brings everything together for retirement and investment.

Transparent pricing

No fine print. Here's exactly what you pay.

Make an appointment

Ready for a modern retirement or wealth solution? Feel free to get to know Vive and discover what's possible - for your organization.

Complex pension, simply explained - know where you are right away

Persoonlijk gesprek voor jouw situatie en die van je werknemers

More clarity than hours of Googling in 30 minutes

Plenty of room for questions to our experienced pension experts

Frequently Asked Questions

Dit zijn de meestgestelde vragen die wij krijgen over pensioen regelen voor je werknemers.

How does the sponsorship of pension accounts work?

Sponsoring employee pensions can be done on a completely voluntary basis. It means that as an employer, you take on a portion of the costs for the Vive service and app for your company. These are the standard costs. The management fee (AuM, Assets Under Management) is paid by the employees themselves.

Is pensioen verplicht voor alle werknemers?

Nee, pensioen is niet verplicht voor alle werknemers. Alleen als je onder een cao valt waarin pensioenopbouw is opgenomen, ben je als werkgever verplicht om een regeling te treffen. Werkgevers zonder cao hebben meer vrijheid. Met Vive kun je pensioen regelen voor werknemers zonder cao op jouw manier – flexibel en persoonlijk. Je hoeft niet iedereen exact dezelfde regeling te geven: je kiest zelf wie je sponsort en hoeveel.

What happens if I take out a subscription?

If you take out a subscription with Vive, we will send a confirmation email with all the registration information. We will then immediately start working on creating your account. For individuals starting to invest via Vive, their account can be set up within 1 hour.

The longer turnaround time may be due to the CDD/KYC check performed after registration. For companies, freelancers (ZZP'ers), or entrepreneurs, accounts with Vive are created within 1-2 working day(s) (excluding weekends). We always try to create an account for you on the same day, however, the CDD/KYC sometimes takes longer.

The lead time from application to implementation can always be discussed. We often see that companies want to wait a bit longer before creating accounts. We see that employers often want to inform their employees in advance about the new employment benefit.

How does Vive protect my assets?

Yes. Your investments are held by an independent custody company, separate from Vive. In the event of bankruptcy, your money remains protected.

What are the pension costs per employee?

What if an employee leaves my employment?

Vive's subscription and pension are designed to be flexibly scaled up and down. If an employee leaves, you simply let us know and we will process in our administration. We will also contact the employee and ensure they are informed of the changes to their subscription.

Please note:

Investing carries risks

Investing offers opportunities, but you may lose part or all of your investment. That’s why it’s important to understand the associated risks in advance. More information can be found in the Investment Policy. Vive is a licensed wealth manager.