Arranging a pension for your employees? This is what you need to know

Offering a pension plan is crucial for attracting and retaining talent in a competitive labour market. Employees regard a good pension scheme as a valuable employment benefit that contributes to their financial security and job satisfaction.

Unfortunately, many employers often postpone arranging a pension for their employees because they find pensions complex and think they are very expensive. But, as this blog will show, this is actually completely untrue! So, have you been putting off arranging a pension for your employees for a while? Then read on quickly.

What are the four pension pillars?

Ugh, pension pillars... Exactly the kind of dry word that makes you not want to read any further. Still, it is important that you know something about this. We will do our best to explain it as simply as possible. But, we cannot promise it will not be boring.

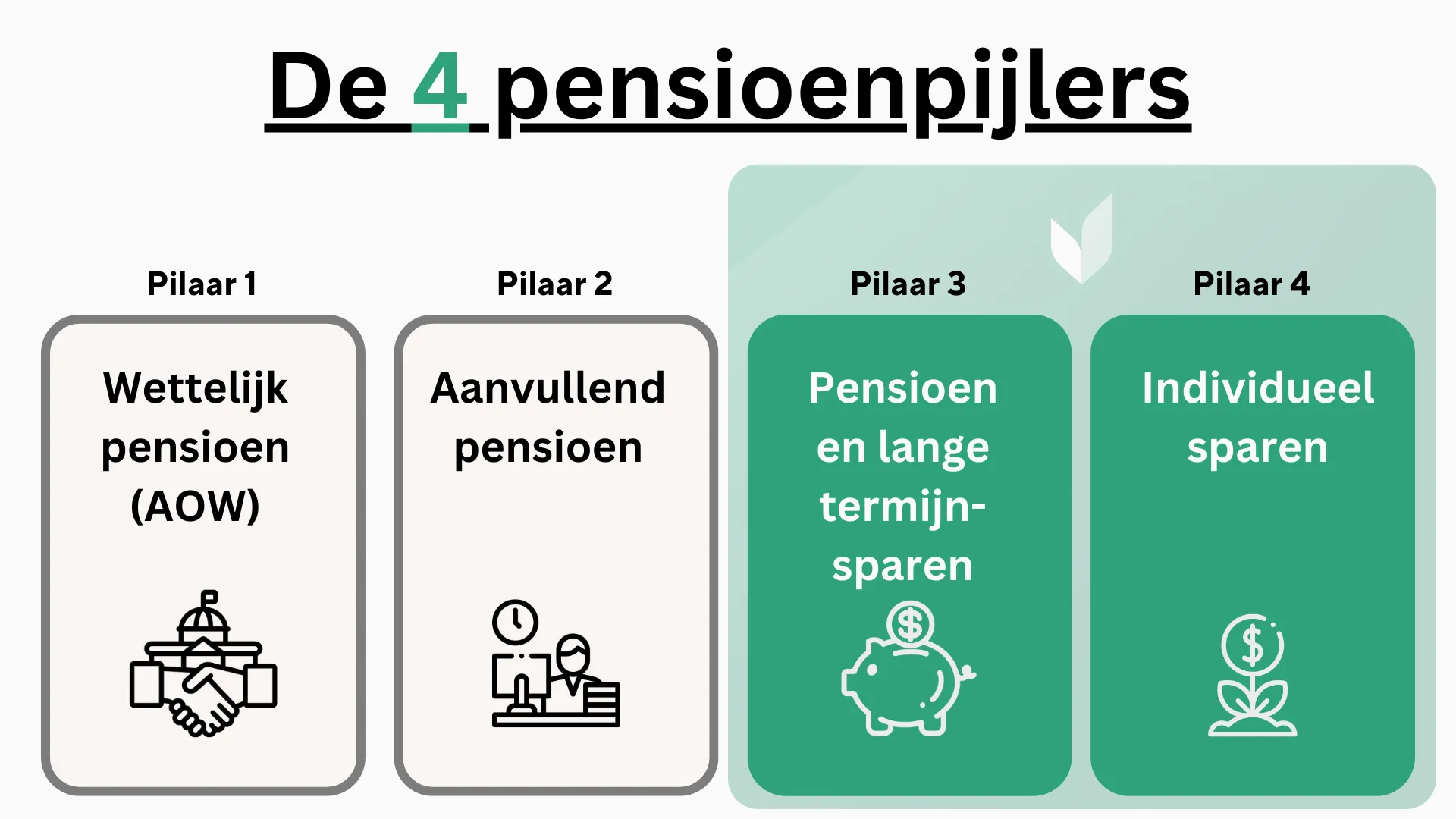

You could see the pension pillars as pots from which employees can build up their pension. These are the pillars:

Pension Pillar 1: AOW (General Old Age Pensions Act)

The first pillar is the AOW, which the government arranges for everyone who lives or has worked in the Netherlands. As an employer, you do not have to do anything with this. AOW provides a basic income that people can rely on after reaching the retirement age. This should amount to approximately 40% of your total pension.

Pension Pillar 2: Pension via the employer

The second pillar is a supplementary pension that is accrued via the employer. In many cases, employers are obliged to arrange this supplementary pension for their employees. This is not the case for around 30% of companies in the Netherlands. These are usually companies that have fewer than 50 employees. From 50 employees, you are obliged to set up a works council, and the first thing they often want is a pension.

Most companies offer a collective pension scheme to which both the employer and the employee contribute. This pillar is crucial for providing a stable income after retirement.

Pension Pillar 3: Supplementary pension (saving and investing yourself)

Employees can save or invest extra themselves to supplement their pension. This can be done via various financial products, such as annuities. This option gives employees more control and flexibility over their pension accrual. For example, they can choose to withdraw money even before their pension, if it turns out they achieve their goals sooner than expected. Or they can have a large amount paid out immediately at the start of their retirement, for example, to take a long trip.

Pension Pillar 4: Pension from own assets

Employees can choose to use assets such as savings, investments, or real estate as a form of pension. This asset can be an important source of income during the retirement years. When you accrue a pension via pillars 2 and 3, you receive a tax advantage. You can deduct the money you set aside for your pension from your income in box 1. You do not have this tax advantage when you accrue a pension via pillar 4.

Now you know what the four pension pillars are, and you immediately know the most important thing. As an employer, you only have to deal with the second pillar. The first pillar is for the government, and the third and fourth pillars are for the employees themselves to arrange as they wish.

But, how do you arrange that second pillar now?

What pension providers are there?

Many employers suffer from procrastination because they think arranging a pension is too difficult and too expensive. As soon as they really cannot avoid it anymore, they immediately run to a large, well-known pension fund such as ABP, Zorg en Welzijn, or Metaal en Techniek (this is naturally not the case if the employer falls under a sector Collective Labour Agreement, then it is mandatory). Or they end up with a pension insurer such as A.S.R., Nationale Nederlanden or Aegon. Precisely these kinds of pension solutions are expensive. Moreover, they offer little flexibility.

The lack of flexibility is simply inherent to a collective pension fund. But nowadays, most employees value the possibility of setting up an individual plan. Fortunately, thanks to new technologies, disruptor pension funds are now also emerging. Because these disruptors have no legacy and work with new technologies, they can offer cheaper and better services.

Moreover, they can offer your employees the option to build up part of their pension via the normal route, namely via pension pillar 2, and at the same time also build up a pension via pension pillars 3 and 4. This allows employees to set goals that suit their future vision. And the only thing you, as an employer, have to do is agree on how much pension you will contribute for your employees. The responsibility for building up the pension therefore lies with the employee. This results in less administrative work for you.

Your employees' pension arranged in four steps

This is how easy you should be able to arrange the pension for your employees, with the right technology:

Step 1: Contact the pension provider.

Step 2: Sign a contract.

Step 3: Provide the contact details of your employees.

Step 4: Decide how much pension you want to contribute for each employee.

Your employee does the rest via an app.

Make an appointment

Ready for a modern retirement or wealth solution? Feel free to get to know Vive and discover what's possible - for your organization.

Complex pension, simply explained - know where you are right away

Personal interview for your situation and that of your employees

More clarity than hours of Googling in 30 minutes

Plenty of room for questions to our experienced pension experts