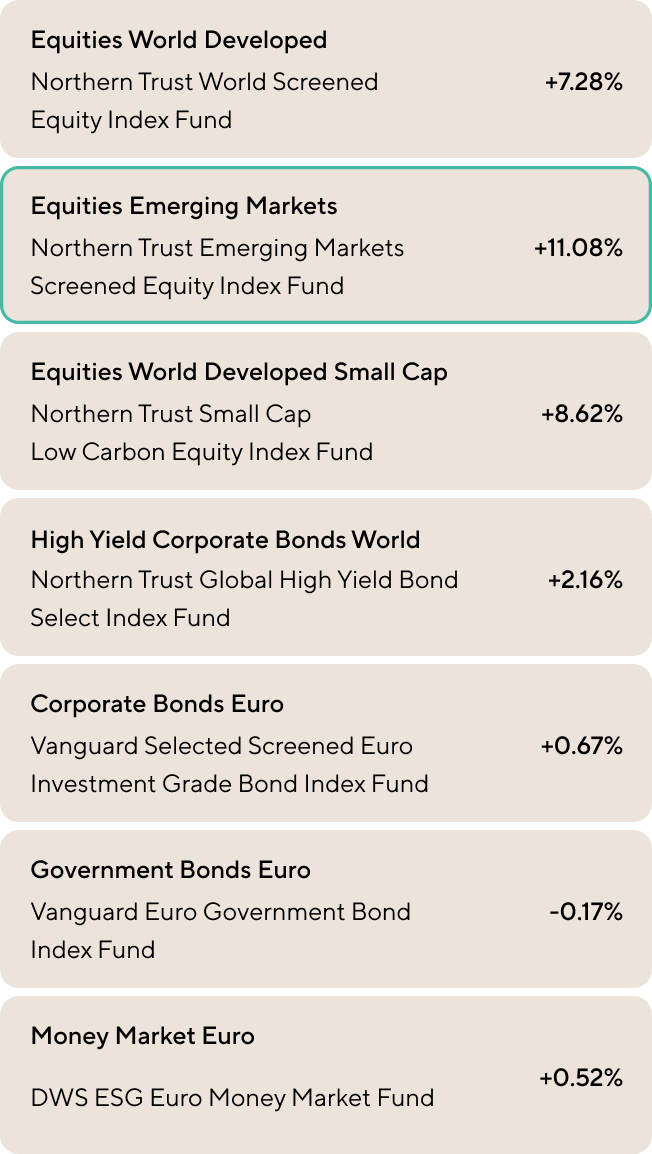

Equity markets in developed and emerging economies showed strong results in the third quarter of 2025. Reduced trade tensions contributed to a more optimistic market sentiment. European government bonds, however, lagged behind, primarily due to political unrest in France.

The third quarter of 2025 brought greater clarity worldwide regarding the proposed import tariffs by the United States. As the August 1st deadline approached, the American government increasingly concluded new deals with trade partners or further postponed the tariffs. This led to more optimism in the market.

Although inflation in the US slightly increased, the American central bank (the Federal Reserve) decided in September to cut the interest rate by 0.25%. This decision followed the most recent jobs report, which showed a sharp decline in the number of new vacancies. The Fed thus balanced between its two core tasks: stimulating economic growth and keeping inflation in check. Despite the risk of higher inflation, the central bank opted for an interest rate cut to stimulate the American economy.

Emerging markets experienced a particularly strong quarter. Even though the threat of import tariffs persisted, the reduced uncertainty led to a rise in stock prices. China, the largest emerging market, also announced extra measures to combat so-called involution. Involution is an exhausting form of hyper-competition in which companies compete each other to death. This occurs in several industries in China, such as the electric vehicle market, where overproduction and price pressure weigh heavily. The announced measures by the Chinese government led to renewed investor confidence.

European government bonds had a less favourable quarter, partly due to political unrest in France. Prime Minister Bayrou lost a vote of confidence and resigned, while the country grapples with a budget deficit of 5% of GDP, the highest within the Eurozone and well above the EU norm of 3%.

Shortly after the political crisis, credit rating agency Fitch lowered France's credit rating from AA- to A+, which put additional pressure on financial markets within the Eurozone.

Political unrest and high national debt in France led to a downgrade of the country's credit status last quarter: from AA- to A+. But what exactly does that entail and what does it mean for you as an investor?

When governments or companies want to borrow money, they often do so by issuing bonds. Credit rating agencies, such as Fitch and Standard & Poor's, assess the likelihood that the issuer will repay their debt. The highest rating, AAA+, indicates a highly reliable borrower. Bonds with a rating up to and including BBB- are considered investment grade, or of investment quality. Below that, we speak of high yield or junk bonds: riskier bonds with an accompanying higher interest compensation.

The lower the rating, the greater the risk that the issuer will not repay. Investors then demand a higher interest rate as compensation. In other words: a bond with a lower credit rating must become cheaper to remain attractive.

For France, the lower rating means that government loans have become riskier in the eyes of investors. At Vive, we partly invest in French government bonds within the Eurozone Government Bond Fund. The decline in value of these bonds resulted in a slightly negative return in this fund this quarter.

The third quarter showed several faces. While global equity markets achieved a solid positive return, other investment categories lagged behind. Whether this positive trend for equities will continue is uncertain. Moreover, it is difficult to capitalise on it.

Therefore, our advice remains unchanged: stick to your strategy.

Do not get carried away by temporary market movements or emotion. Stay focused on your personal financial goals. Only adjust your portfolio if your personal situation changes and not because of the whims of the market.

A broadly diversified, systematically managed strategy, like Vive's, offers the best basis for long-term success. Trust the process and let your strategy work for you.